Questions Every Investor Should Ask Before Committing Capital

Most investment decisions begin with a simple question.

How much could this return?

That question is understandable.

Returns are visible.

They are easy to compare.

They make investment choices feel measurable.

But before committing capital, a different set of questions often matters just as much.

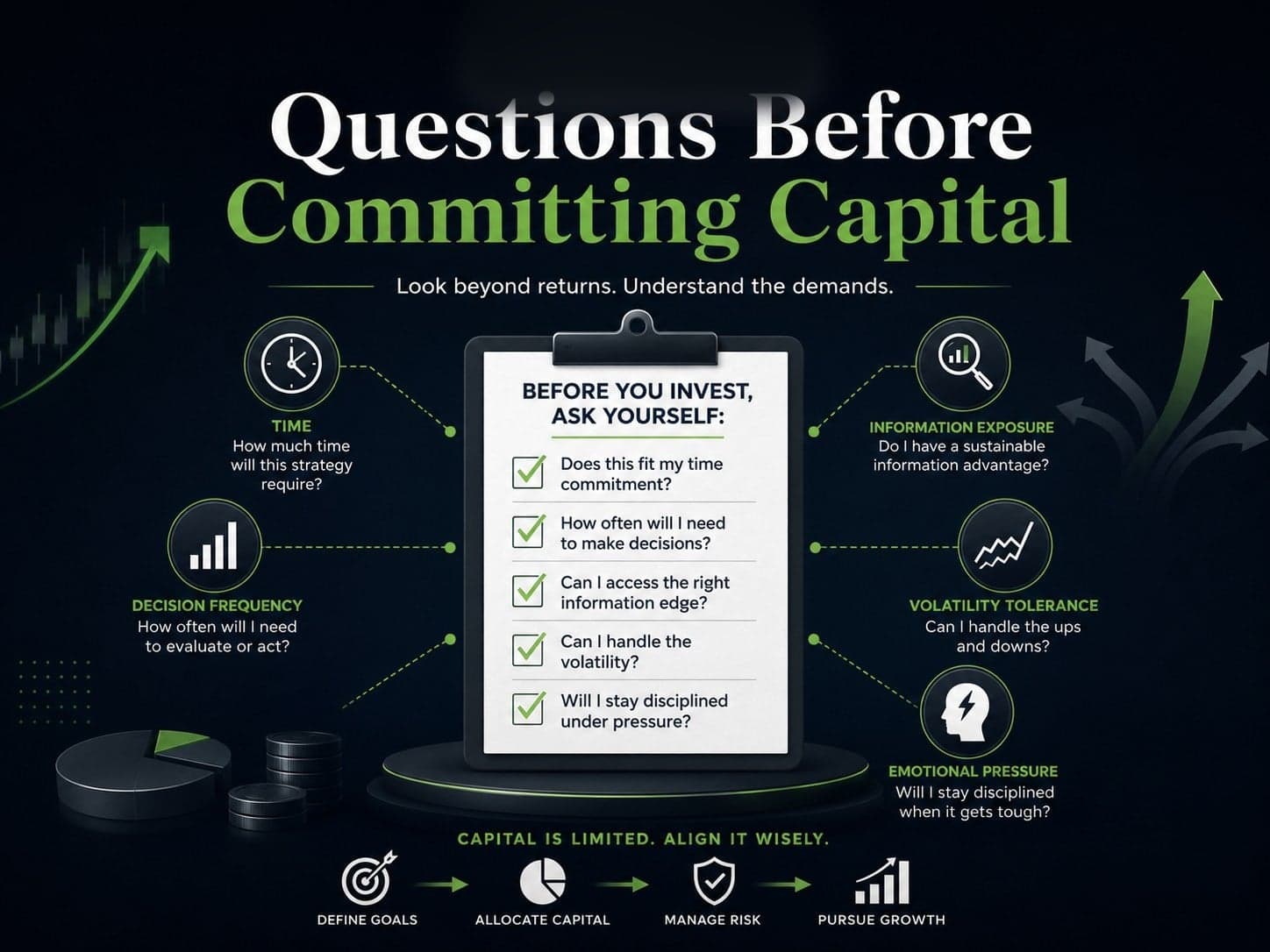

- What will this investment require over time?

- How much attention will it demand?

- How often will decisions need to be made?

- How much uncertainty must be tolerated before the outcome becomes clear?

Capital is committed in a moment.

The demands of that commitment are lived over time.

This is why questions before committing capital should not focus only on expected returns, risk categories, or headline performance. They should also examine the structure behind the investment and the behavioral demands that structure may create.

The question is not only what an investment might deliver.

It is what it will ask the investor to sustain.

Why Capital Commitment Creates More Than Financial Exposure

Committing capital is often treated as a financial action.

- Money is allocated.

- A position is opened.

- An investment is selected.

But in practice, capital commitment also creates exposure to an ongoing environment.

That environment may include:

- Information updates

- Price movement

- Uncertainty

- Decision pressure

- Periods of doubt

- Delayed feedback

The financial commitment may happen once.

The behavioral commitment continues.

This distinction matters because many investment difficulties do not appear at the moment capital is committed. They appear later, when the investor has to continue living with the structure they entered.

A structure that looked reasonable at the beginning may later require more time, attention, interpretation, or emotional endurance than expected.

That is why committing capital without understanding structural demand can create friction long before the investment outcome is clear.

Direct Answer

What questions should investors ask before committing capital?

Investors should ask how much time, attention, decision-making, information exposure, volatility tolerance, and emotional endurance an investment structure may require over time.

These questions do not predict outcomes.

They help reveal the demands that may remain hidden when an investment is evaluated only by expected return.

Before You Commit Capital, Ask:

The Questions Returns Cannot Answer

Returns summarize outcomes.

They do not explain the experience required to reach those outcomes.

A return figure does not show:

- How often the investor must monitor the investment

- How much information must be interpreted

- How frequently decisions may be required

- How long uncertainty may persist

- How emotionally difficult volatility may feel

- How easily the investment fits into daily life

This is why comparing investments only by return can create a misleading sense of clarity.

Two investments may appear similar on paper but impose very different demands in practice.

One may require continuous attention.

Another may require patience and restraint.

One may produce frequent decision points.

Another may require long periods of inaction under uncertainty.

The difference may not appear in performance summaries.

It appears in the conditions the investor must sustain.

This is the deeper reason a broader investment comparison framework matters: it helps separate what an investment may deliver from what it may demand.

Questions About Time, Attention, and Information Exposure

Before committing capital, investors should ask what kind of informational environment they are entering.

Not all investments require the same level of attention.

Some structures expose the investor to frequent updates, visible price movements, ongoing signals, and constant comparison. Others operate with lower visibility and fewer required interactions.

Useful questions include:

- How often will this investment require my attention?

- How frequently will new information appear?

- How much of that information will need interpretation?

- Will I need to monitor this actively or periodically?

- Will visibility help me stay informed, or increase pressure to react?

These questions matter because information does not only inform decisions.

It can also create cognitive demand.

High information exposure can increase the need to filter signals, interpret noise, and repeatedly reassess uncertainty. Over time, that exposure may become a structural burden rather than a source of clarity.

This connects directly to information density in investing, where the issue is not simply how much information exists, but how much of it the investor is required to process in order to remain engaged.

The key question is not:

Do I have enough information?

It is:

How much information will this structure require me to live with?

Questions About Decision Frequency and Behavioral Pressure

Some investments require occasional evaluation.

Others create repeated decision points.

Before committing capital, investors should ask how often judgment will be required.

Useful questions include:

- How often will I need to make decisions?

- Which decisions are predefined, and which are discretionary?

- What happens if I delay a decision?

- Will this structure require frequent adjustment?

- Could repeated judgment become difficult to sustain?

Decision frequency matters because every decision consumes cognitive bandwidth.

A single decision may feel manageable.

A repeated pattern of decisions can become draining.

This is especially important in structures where the investor must constantly decide whether to hold, adjust, rebalance, exit, add, reduce, or reinterpret new information.

The issue is not whether the investor is capable of making decisions.

The issue is whether the structure requires more decision-making than the investor can sustainably carry over time.

That is why decision fatigue in investing is not merely a psychological issue. It can be a structural consequence of repeated decision exposure.

A good question does not remove uncertainty.

It makes hidden demands visible before they become pressure.

Questions About Volatility, Time Horizon, and Endurance

Volatility is often discussed as a number.

But investors do not experience volatility only as a number.

They experience it as movement, uncertainty, delay, discomfort, and sometimes doubt.

Before committing capital, investors should ask:

- What kind of volatility could this structure expose me to?

- How visible will that volatility be?

- How long might discomfort last?

- Can I remain aligned if outcomes take longer than expected?

- Does this structure match my actual time horizon?

The time horizon question is especially important.

Many investors say they are long-term.

But the structure they choose may expose them to short-term feedback, frequent updates, and constant comparison.

This creates a mismatch.

The investor may believe they are making a long-term commitment while living inside a short-term evaluation environment.

That gap can make patience harder to sustain.

This is closely related to time horizon mismatch in investing, where the stated horizon and the experienced horizon are not the same.

Before committing capital, the investor should not only ask:

How long can I invest?

They should ask:

How often will this structure make me feel like I need to reconsider?

Questions About Fit Before Commitment

An investment can make sense on paper and still create friction in real life.

That friction may come from time limits, emotional capacity, work pressure, family obligations, lack of attention, or low tolerance for constant monitoring.

Before committing capital, investors should ask:

- Does this investment fit my daily reality?

- Can I maintain this structure when life becomes busy?

- Will this require attention I may not consistently have?

- Can I tolerate the uncertainty this structure creates?

- What happens if stress outside the market increases?

These questions do not decide whether an investment is good or bad.

They clarify whether the investment structure fits the conditions under which the investor actually lives.

This connects directly to how to know if an investment fits your life. Investment fit is not only about goals, returns, or risk labels. It is also about whether the structure can be sustained under real conditions.

Commitment risk is not only financial.

It is also structural and behavioral.

Questions About Responsibility and Control

Capital commitment also changes responsibility.

Some structures place more responsibility on the investor.

They require active monitoring, interpretation, timing, adjustment, and ongoing judgment.

Other structures distribute responsibility differently.

They may use rules, automation, professional management, index exposure, delegation, or predefined processes to reduce direct intervention.

Before committing capital, investors should ask:

- What am I personally responsible for after entering this investment?

- Which decisions remain with me?

- Which decisions are handled by the structure?

- What level of control do I actually need?

- Does more control also mean more pressure?

This distinction matters because control can feel attractive before commitment.

But over time, control may become responsibility.

The investor may not only have the ability to act.

They may feel pressure to act.

In trading environments, this distinction becomes even more visible because monitoring, execution, and repeated decision-making can create demands long before performance is fully understood.

The question is not whether control is good or bad.

The question is whether the investor wants the ongoing responsibility that comes with that control.

This becomes especially important when comparing active, passive, delegated, or automated investment structures.

Why Better Questions Do Not Guarantee Better Outcomes

Asking better questions does not guarantee better investment results.

It does not remove risk.

It does not predict performance.

It does not eliminate uncertainty.

But it can reduce a specific kind of mistake:

Entering a structure without understanding what it may require.

Better questions help investors see the difference between:

- Expected return and lived experience

- Financial exposure and behavioral exposure

- Initial confidence and long-term sustainability

- Stated tolerance and real endurance

This matters because many investment breakdowns are not caused by a lack of intelligence.

They happen because the structure creates demands the investor did not anticipate.

The goal of better questioning is not certainty.

The goal is visibility.

Where This Leads Next

Once the demands of an investment structure become visible, another question naturally appears.

Does the investor need to carry all of those demands personally?

Some structures require direct control and ongoing judgment.

Others distribute responsibility through rules, systems, delegation, automation, or external decision frameworks.

This does not remove responsibility.

It changes where responsibility sits.

That is why the next step in this discussion is not only about asking better questions before committing capital.

It is about understanding delegation.

Not as avoidance.

Not as blind trust.

But as a different way to manage control without constant stress.

Frequently Asked Questions

What questions should I ask before committing capital?

Before committing capital, investors should ask what an investment may require in time, attention, decision-making, information exposure, volatility tolerance, and emotional endurance. These questions help reveal structural demands that may not appear in return comparisons.

Why should investors look beyond returns before investing?

Returns describe possible outcomes, but they do not show the experience required to reach those outcomes. Investors may need to consider decision frequency, uncertainty, information exposure, and behavioral pressure before committing capital.

What does capital commitment mean in investing?

Capital commitment means allocating money to an investment structure. In practice, it also creates ongoing exposure to uncertainty, monitoring, decisions, volatility, and the behavioral demands of staying aligned over time.

How can investors evaluate investment fit before committing?

Investors can evaluate fit by asking whether the investment structure matches their available time, attention, emotional capacity, risk tolerance, and ability to remain aligned during uncertainty.

Can better questions reduce investment mistakes?

Better questions cannot guarantee better outcomes, but they can make hidden demands more visible before capital is committed. This may help investors recognize structural mismatches earlier.

Why does decision frequency matter before investing?

Decision frequency matters because repeated decisions can create cognitive strain over time. An investment that requires frequent judgment may be harder to sustain than one with fewer decision points, even if the expected outcome appears similar.

Closing Insight

Committing capital is easy to define.

It is harder to live with.

The most important questions are not only about what an investment might return.

They are about what the investment will require when uncertainty appears, attention is limited, and decisions become harder to sustain.

Capital enters first.

Structure follows the investor over time

And over time, structure determines what the investor must continue to carry.